Raleigh Fee-Only Financial Planner Mike Palmer in Kiplinger: A Navigation Guide to the 2026 Tax Playbook for Carolinas Executives

How to avoid some tax traps within the OBBBA targeting executive compensation.

If you are a corporate executive or business owner living in the Research Triangle (Raleigh) or the Queen City (Charlotte), your compensation structure is likely far from standard. Between vesting Restricted Stock Units (RSUs), Incentive Stock Options (ISOs), deferred compensation, and performance bonuses, a substantial percentage of your wealth is tied directly to complex tax rules.

In his recent Kiplinger column (A 2026 Tax Playbook for High Earners: Stealth Taxes and Strategic Wins) Raleigh fee-only planner Mike Palmer shares strategies for navigating these complexities. With the passage of the One Big Beautiful Bill Act (OBBBA), the financial playing field has shifted dramatically. While it permanently locked in several favorable rules, it simultaneously set up "stealth tax traps" that specifically target high-earning professionals.

At Ark Royal Wealth Management—a fee-only, fiduciary wealth advisory firm with offices in Raleigh and Charlotte—we believe in coordinating every element of your financial life to help you make smart, intentional choices with your money.

Here is your 2026 Executive Tax Playbook to help you preserve your hard-earned wealth.

Part 1: The OBBBA Permanent Victories

First, the good news. The OBBBA resolved much of the uncertainty surrounding the expiration of the Tax Cuts and Jobs Act (TCJA). For North Carolina's high-income earners, these permanent victories bring critical stability to long-term planning:

Top-Rate Stability: The top federal ordinary income tax rate is now permanently capped at 37%. Without this law, the top bracket was scheduled to revert to 39.6% in 2026.

QBI Deduction: The 20% Qualified Business Income (QBI) deduction for pass-through entities (S-corps, LLCs, and partnerships) is now permanent, which is a massive win for consulting business owners and independent executives across Raleigh and Charlotte.

Massive Estate Exemption: The federal estate tax exemption is locked in at $15 million per person ($30 million for married couples) through 2033. This provides a highly favorable window for wealth transfer planning.

100% Bonus Depreciation: The OBBBA permanently restored 100% first-year bonus depreciation, allowing immediate deduction of business equipment costs.

Part 2: The 4 "Stealth Traps" Targeting Your Compensation

While the permanent provisions are substantial, the OBBBA introduced severe limitations that act as an effective "stealth tax" on executive compensation. If you do not plan ahead, a single $75,000 corporate bonus in 2026 could actually lower your net take-home pay by triggering phase-outs.

Here are the four key traps we are actively helping clients navigate:

1. The SALT Cap Phase-Out

While the OBBBA raised the State and Local Tax (SALT) deduction cap to $40,400 for joint filers, it added a steep income-based cliff.

The Trap: This expanded cap only applies to joint filers with a Modified Adjusted Gross Income (MAGI) under $505,000. Once your MAGI climbs past this limit, the deduction phases out entirely and reverts to the old $10,000 limit by the time you hit $600,000.

The NC Workaround: For corporate leaders and business owners, utilizing Nonqualified Deferred Compensation (NQDC) plans can strategically defer current taxable income. For business owners, electing North Carolina's Pass-Through Entity Tax (PTET) allows your business to pay state income taxes at the entity level, bypassing the SALT limit entirely.

2. The 2026 Alternative Minimum Tax (AMT) Reset

The Trap: The AMT exemption has dropped significantly in 2026. For married filers, the exemption resets to $140,000. Compounding this, the exemption phase-out rate has doubled from 25% to 50%.

The Strategy: If you plan to exercise Incentive Stock Options (ISOs) this year, the spread between the grant price and the fair market value is treated as an AMT preference item. Failing to run an AMT projection prior to exercising could result in a devastating tax surprise next April.

3. The Charitable "Cover Charge"

The Trap: Charitable donations face a new floor in 2026. You can now only deduct charitable gifts that exceed 0.5% of your Adjusted Gross Income (AGI). If your AGI is $800,000, your first $4,000 in donations yields zero tax benefit.

The Strategy: Instead of making smaller, annual cash gifts, employ a bunching strategy. By making a single, larger contribution (such as $50,000) to a Donor-Advised Fund (DAF) in a high-income year, you easily clear the 0.5% floor and secure a highly impactful tax deduction while retaining the ability to grant those funds to charities over several years.

4. The 2/37ths Deduction Limit

The Trap: If your income lands you in the top 37% tax bracket, the OBBBA caps the value of your itemized deductions to 35 cents on the dollar.

The Strategy: Because of this 2% gap, "above-the-line" deductions are more valuable than ever. Maximizing pre-tax contributions to your 401(k) and Health Savings Account (HSA) reduces your AGI before this itemized cap is even calculated.

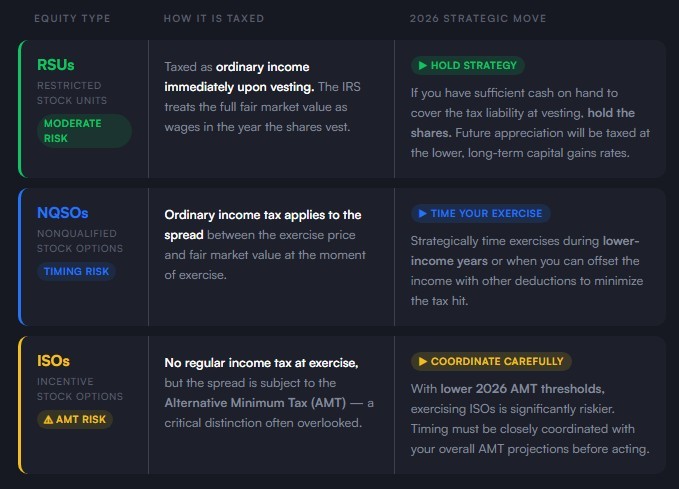

Part 3: Mastering Your Equity Compensation

Equity is often the engine of an executive's net worth, but it is also the most complex. To illustrate the ideal tax treatment of different equity structures, we have broken down how they behave under the 2026 tax code:

A Warning on Overconcentration: Many executives in Charlotte's banking corridor and Raleigh's tech hub face pressure to hold substantial company stock to signal confidence to the market. This often leads to overconcentration. Securing a diversified, resilient portfolio is crucial to long-term wealth preservation.

Part 4: Advanced Wealth Coordination

To keep more of what you earn, look beyond the standard pre-tax retirement limits:

1.Evaluate the Mega Backdoor Roth (For High Savings Capacity)

If your corporate retirement plan allows for after-tax contributions, you can potentially funnel up to an additional $47,500 into a Roth 401(k) for 2026 (staying within the total IRS limit of $72,000). These funds grow and can be withdrawn completely tax-free.

2.Deploy the PTET Workaround (For Business Owners & Consultants)

If you have consulting revenue or own a local business in North Carolina, utilize the Pass-Through Entity Tax (PTET) election. Paying state tax at the business entity level successfully bypasses individual SALT income caps.

3.Model Nonqualified Deferred Compensation (NQDC) (Watch Section 409A Closely)

NQDC plans allow you to defer earning salary and bonuses—and avoid the immediate 37% federal tax hit—until retirement when you will likely be in a lower tax bracket. However, these plans are strictly bound by Section 409A rules. A single improper election can trigger a devastating 20% excise tax penalty.

Partnering with a Carolinas Fiduciary

Tax, equity, and retirement strategies cannot be managed in silos. An adjustment to your deferred compensation plan changes your AGI, which impacts your charitable deduction floor, which in turn influences your AMT exposure.

At Ark Royal Wealth Management, we serve as your financial compass. As fee-only, fiduciary Certified Financial Planner™ (CFP®) professionals based in Raleigh and Charlotte, we never sell products or earn commissions. Our sole objective is to align your investments, equity, and tax planning into one seamless, wealth-preserving strategy.

Don't leave money on the table in 2026. Let's coordinate your wealth plan together.