Maximizing Your Wealth: Is a Mega Backdoor Roth Right for High Earners in Raleigh & Charlotte?

Even if you can't do a Backdoor Roth IRA, you may still be able to leverage the power of a Mega Backdoor Roth in your 401k.

For high-income earners in North Carolina's booming financial and tech hubs—from the banking centers of Uptown Charlotte to the innovation corridors of Raleigh and the Research Triangle—maximizing retirement savings requires exploring creative strategies.

Many high income earners fall outside of the income phaseout ranges to make direct Roth IRA contributions. For 2026 the modified adjusted gross income (MAGI) limits are as follows:

SIngle / Head of Household: $153,000 - $167,999

Married Filing Jointly: $242,000 - $251,999

Just because your income is above these thresholds doesn't preclude you from making a backdoor Roth IRA contribution, as we explain in more detail below. However, what's often overlooked as a powerful strategy (provided your employer’s retirement plan allows it) is the Mega Backdoor Roth.

At Ark Royal Wealth Management, we help high-net-worth families navigate complex tax codes to build lasting, tax-efficient legacies. Here is everything you need to know about how this advanced wealth-building tool works.

Understanding the Standard Backdoor Roth

To appreciate the scale of a Mega Backdoor Roth, it helps to first look at the standard backdoor Roth IRA.

Normally, the tax code places strict income limits on direct Roth IRA contributions. For instance, if you are single and your income exceeds $153,000, you are legally restricted from making a direct contribution. To bypass this restriction, high earners can utilize a "workaround":

Make a nondeductible, after-tax contribution to a traditional IRA (which has no income caps for after-tax contributions).

Immediately convert those funds into a Roth IRA.

The Power of Eliminating "Tax Drag"

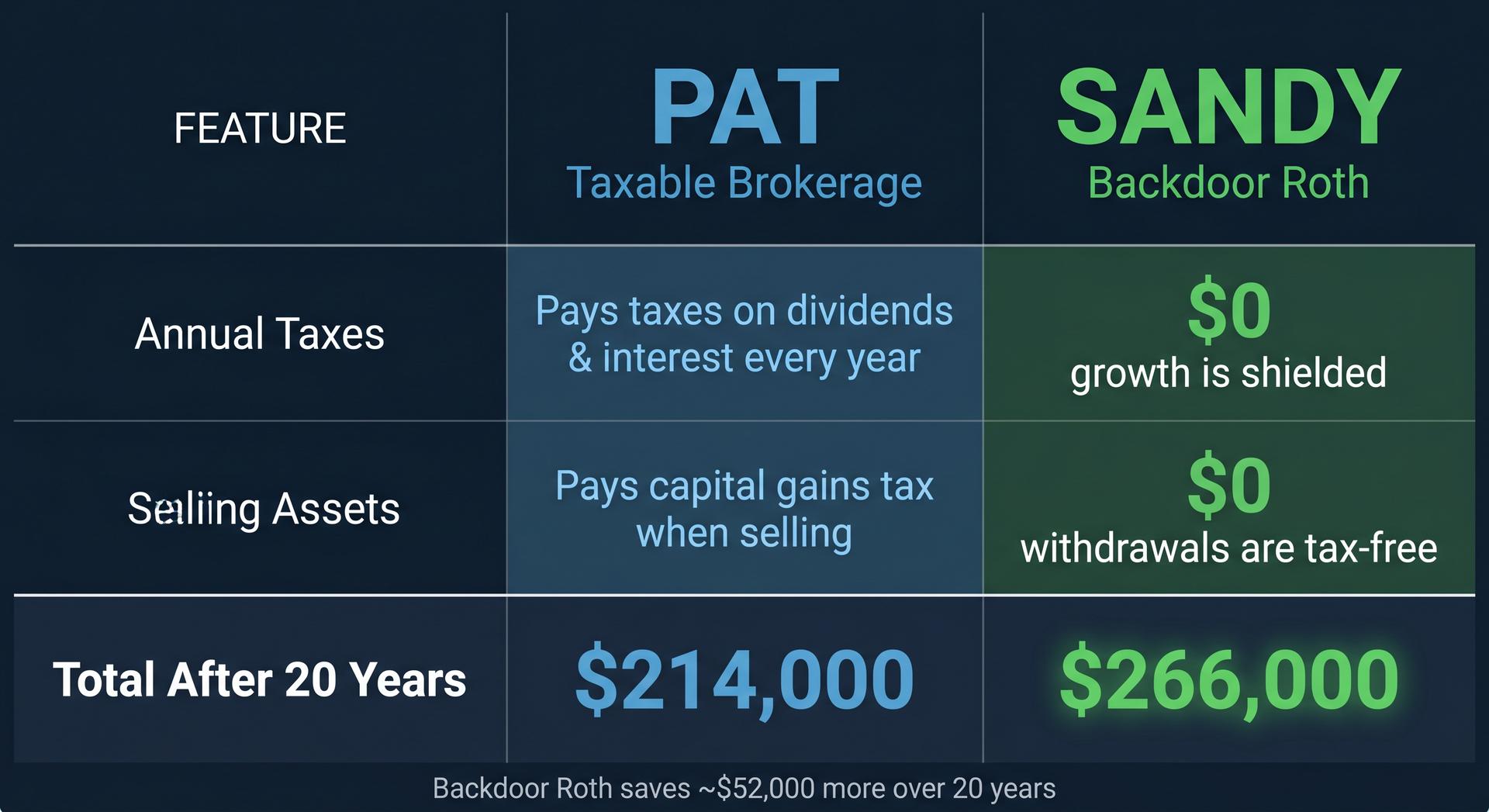

To see why this matters, consider a 20-year investment horizon comparing two high-earning investors, Pat and Sandy, who each have an extra $7,500 to invest annually (the 2026 standard IRA contribution limit). Both are in a 24% tax bracket.

Pat (Taxable Brokerage Account): Pat invests via a standard brokerage account. Every year, a portion of her returns is chipped away by taxes on dividends, interest, and portfolio rebalancing. After 20 years, her account grows to about $214,000—and she will still owe significant capital gains taxes when she withdraws it.

Sandy (Backdoor Roth IRA): Sandy uses the backdoor Roth strategy. Her money grows entirely shielded from annual taxes, allowing the full balance to compound. After 20 years, Sandy ends up with about $266,000—roughly $52,000 more than Pat—and every dollar of it can be withdrawn completely tax-free.

Additionally, because Roth IRAs are exempt from Required Minimum Distributions (RMDs) during the owner's lifetime, Sandy can let this money grow indefinitely or pass it to her heirs entirely tax-free.

Note: The standard backdoor Roth gets complicated if you already hold pretax funds in a traditional IRA. The IRS applies the pro-rata rule to determine how much of the conversion is taxable, which can lead to unintended tax penalties without careful planning.

Leveling Up: The Mega Backdoor Roth

While saving $7,500 a year (or $8,600 if you are age 50 or older) is beneficial, high-performing executives and business owners in Charlotte and Raleigh often want to save far more aggressively.

This is where the Mega Backdoor Roth comes into play by leveraging the significantly higher contribution limits of a corporate 401(k) plan.

In 2026, the standard employee elective deferral limit for a 401(k) is $24,500. However, the IRS allows the total contribution limit—which combines your elective deferrals, your employer’s matching contributions, and additional after-tax contributions (also known as non-deductible contributions)—to reach as high as $72,000 per year (and even higher for those eligible for 50+ catch-up contributions).

If your company's 401(k) plan permits it, you can maximize your standard 401(k) contributions, secure your employer match, and then fill the remaining gap up to the $72,000 limit with separate after-tax contributions.

Once those after-tax dollars are in the plan, you execute the "mega backdoor" step: converting those funds into a Roth IRA or a Roth 401(k). Because you have already paid income tax on the initial after-tax contributions, the conversion itself triggers no additional taxes.

The Power of Scale

Think about the trajectory this creates. Stashing away up to $72,000 a year means that after just 10 years, you could accumulate $720,000 in principal alone; over 20 years, that scales to more than $1.4 million—all compounding entirely tax-free and completely insulated from RMDs.

Critical Pitfalls to Avoid

Because the Mega Backdoor Roth involves moving substantial amounts of capital through specific legal channels, do-it-yourself mistakes can easily trigger severe IRS penalties or thousands of dollars in unnecessary taxes.

Some of the most common oversights include:

Delayed Conversions: If you wait too long to convert your after-tax contributions, those funds will generate investment earnings within the account. Those intermediate earnings become fully taxable upon conversion. Converting as quickly as possible is essential to minimize or avoid taxable gains.

Mixing Plan Buckets: Confusing or improperly blending pretax, standard Roth, and after-tax contributions can create massive accounting and tax headaches during a rollover.

Exceeding Total Limits: Because the $72,000 ceiling fluctuates based on variable employer matching and your own fluctuating contributions, tracking the exact math is vital. Overcontributing can result in severe tax penalties.

Is Your Retirement Plan Eligible?

The biggest catch with the Mega Backdoor Roth is that not all 401(k) plans support it. To utilize this strategy, your employer's plan must explicitly allow both after-tax contributions (which are distinct from Roth contributions) and in-service distributions or in-plan Roth conversions.

Many major employers throughout the Research Triangle (Raleigh/Durham) and the financial services sector in Charlotte offer these advanced features, but plan documents must be reviewed carefully to ensure compliance.

Partner with a Fee-Only Fiduciary Advisor in North Carolina

The Mega Backdoor Roth is a highly sophisticated wealth-management tool that offers immense rewards for those who execute it effectively.

At Ark Royal Wealth Management, we operate as fiduciaries, meaning our advice is always aligned strictly with your best financial interests. We work closely with high-income professionals across Raleigh and Charlotte to analyze corporate benefits packages, optimize annual tax brackets, and construct customized, comprehensive wealth plans.

Are you ready to see if your employer's plan qualifies for a Mega Backdoor Roth, or want to ensure your current retirement strategy is fully optimized for tax-free growth?

Contact Ark Royal Wealth Management today to schedule a consultation.