Unlocking Homeownership: A Guide to NC Down Payment Assistance for Raleigh & Charlotte Buyers

A variety of programs help new NC homebuyers make the dream of homeownership a reality.

If you’ve dreamed of buying a home in Raleigh, Charlotte, or across the vibrant communities of North Carolina, the 2026 spring season brings more than just blooming dogwoods—it brings a significant financial opportunity. At Ark Royal Wealth Management, we help clients navigate complex financial milestones, and for many, planting roots in the Tar Heel State is a top priority.

The NC 1st Home Advantage Down Payment program is currently offering a major perk: $15,000 in down payment assistance for homes priced up to $495,000.

How the $15,000 Forgivable Loan Works

The program functions as a 0% interest, deferred second mortgage. It is designed to bridge the gap between rising local home prices and salaries. However, there is a specific timeline for forgiveness you should understand:

Years 1–10: You owe the full $15,000 if you sell the home or move out.

Years 11–15: The loan is forgiven at a rate of 20% per year.

After Year 15: The debt is 100% forgiven.

Note: If you move or sell before the 15-year mark, you may be responsible for repaying the unforgiven portion and any associated taxes.

Eligibility Requirements for 2026

To qualify, you must secure a 30-year fixed-rate mortgage (FHA, VA, USDA, or conventional); 15-year terms are not eligible for this program. Buyers must also meet these four criteria:

Buyer Status: You must be a first-time homebuyer (haven't owned a primary residence in 3 years) or a U.S. military veteran.

Credit Score: A minimum score of 640 is required (660 for manufactured homes).

Property Value: Generally, the home price must be under $495,000.

Income Limits: Your annual household income must fall below specific limits based on your county and household size.

The "Marriage Penalty" Planning Tip

Income limits vary by location. For example, a couple buying in Wake County (Raleigh) must have a combined income under $152,000. Metropolitan areas like Raleigh, Durham, and Charlotte have higher income thresholds. Check out the NC Housing Finance Agency website for more info.

For couples planning to marry, it may be financially advantageous for one partner to purchase the home individually prior to the wedding. Once married, the NCHFA considers your combined total income, which could push you over the eligibility threshold.

Tax Implications and Benefits

Understanding the tax landscape is vital for long-term wealth management.

Federal/State Income Tax: The IRS and the State of North Carolina generally do not treat state-led forgivable down payment assistance as taxable income.

SALT Deductions: In 2026, itemized filers can deduct property and state income taxes up to $40,400. This is particularly beneficial for those buying in higher-tax areas like Raleigh, Durham, or Charlotte.

Mortgage Credit Certificate (MCC): You may also be eligible for the NC Home Advantage Tax Credit, which allows you to claim 30% to 50% of your annual mortgage interest (up to $2,000) as a direct federal tax credit.

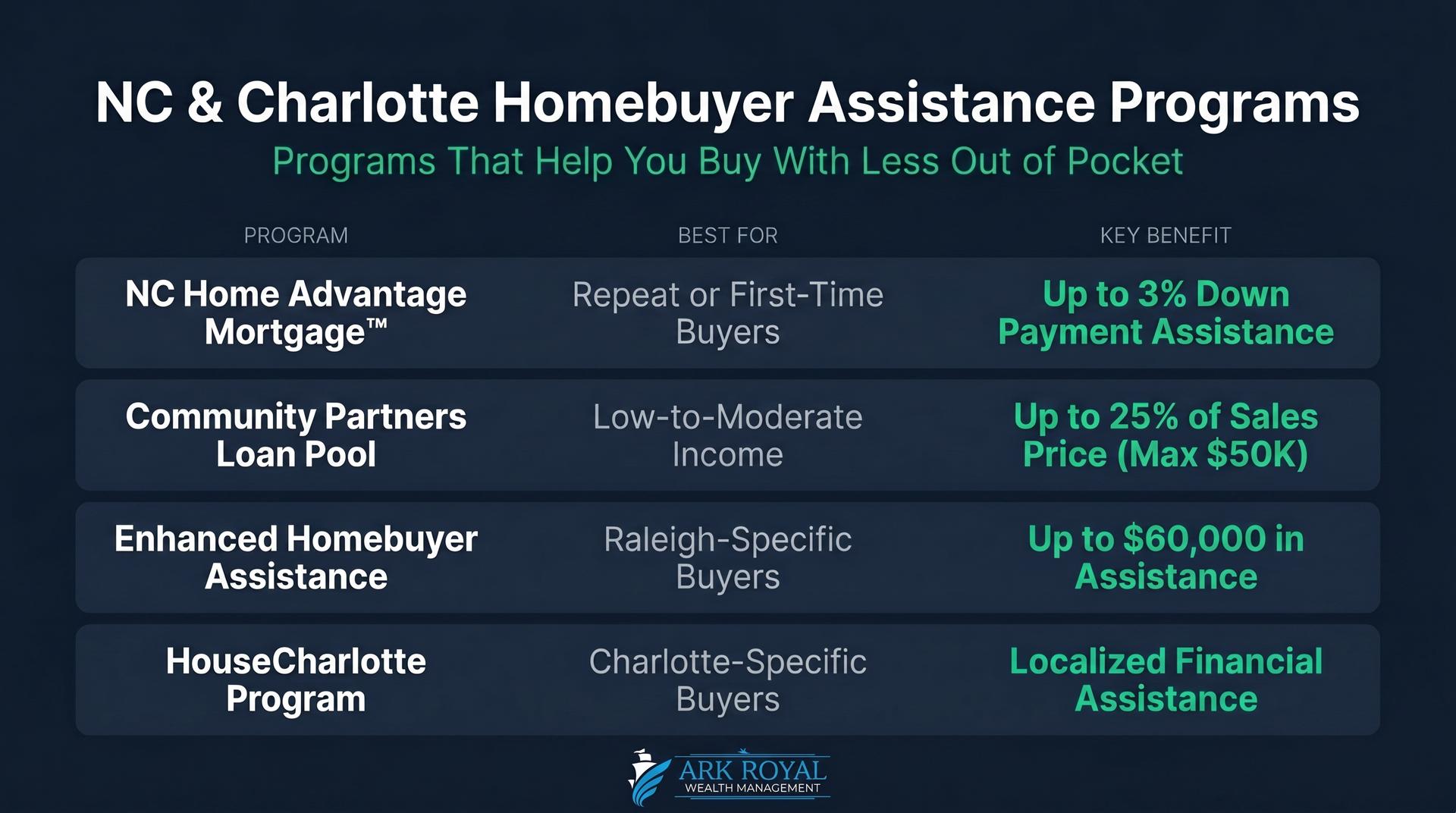

Additional North Carolina Home Purchase Programs

Taking the Next Step

There is no need for a government appointment to start. You can apply through participating private lenders in North Carolina. We recommend searching the NCHFA website for "preferred lenders" in your specific county to ensure you are working with a professional familiar with these incentives.

At Ark Royal Wealth Management, we believe a home is more than just a place to live—it's a pillar of your financial future.